A notable

development these last few weeks has been the change of forward guidance coming

from the Federal reserve. The Fed has gradually turned away from indicating that

they will have 4 instances of rate hikes. This “dovish” talk has caused the

dollar to lose value (relative to global currencies), which means capital may

flow into the US and equities can only hope for better performance in coming

quarters. First quarter earnings results have been terrible for corporate US.

I’ve

been following the negative developments in Venezuela and the following has

happened :-

1.

The country is facing runaway inflation, Zimbabwe-style.

Inflation

has forced the government to use up its now dwindling cash reserves. Unofficial

data indicates an annualised inflation rate of 397.4%

The

government will no longer be able to afford printing money yet the President

still denies inflation.

Mr. Maduro

recently imposed a 2-day work-week for public servants in Venezuela arguing

that keeping them home would save energy.

2.

In the face of the low oil prices, the economy is

expected to shrink by 8% this year.

3.

There’s a real negative turn that seems to be only

getting worse by the days.

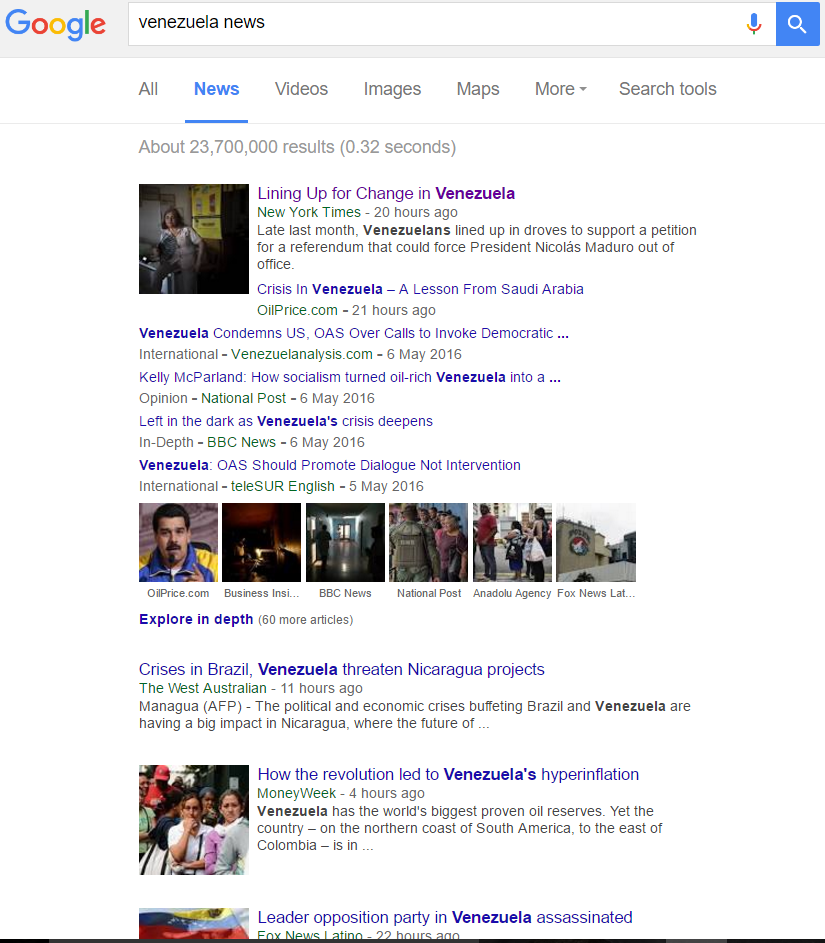

Searching

Venezuela news on Google right now (09/05/26) will bring up news of a people

working to oust Maduro in a referendum petition. A story

that is currently fresh on Reddit will appear that the leader of a regional

opposition party leader has only just been assassinated. It gets very grim very

quickly down the search results but we can only hope for the best for the

people of Venezuela.

In a tide of

social unrest that’s getting underway, people are getting desperate for basic

necessities like food and medicine.

I expound on

a few global risk items and concerns to watch for in the coming quarters as

highlighted initially by Preston of The Investors Podcast :-

1.

The impact

of negative rates for banks in Europe (Particularly Deutsche Bank)

As I’ve written

previously, negative rates are still quite a ‘new’ phenomenon and their effects

on the financial markets is one that we have to continually keep watch on. How

long will banks in Europe sustain having to pay central banks to hold their excess reserves?

How much new lending are banks actually doing? How long will banks accept eroded

profits? How much longer will inflation remain low in Europe? Answers to these questions are still developing and so we wait.

2.

A strong Yen

pushing Japanese stock prices lower

Japanese stocks and

exports that depend on a weak yen are being hammered. The recent major earthquakes in Japan have necessitated a postponement of the tax hike that's expected to be coming Japan's way as well as a delayed early election possibility.

3.

Chinese

Commodity prices returning to reality (because the PBOC pushed commodity prices

into outer space during the first quarter)

Action by the PBOC to

pump credit into the Chinese economy is a definite watch. The image below

courtesy of Stan Druckenmiller through Zero Hedge tells very many stories. A fact for the day from

Stan on China would be, “since 2012 the Chinese banking sector has allowed

credit to grow by the amount of the entire Brazilian GDP per year!”

4.

Potential

impacts of the Saudi currency de-pegging from the US dollar due to the speed

and impact of their domestic reserves being spent. Could cause the dollar

to strengthen and put more pressure on US Stocks.

Given that

Saudi’s 80% revenue is oil-dependent, prolonged low prices in oil may break

Saudi’s peg to the USD some way or another. Although still quite an unlikely

event given their still ‘deep’ reserve pockets, markets are pricing a riyal

devaluation very highly at the moment, as the Bloomberg currency forward image

showed (December 2015). If the Saudi riyal is de-pegged or loosened, the

impacts to the global economy would certainly be catastrophic given their

position as the biggest OPEC member. The reason Saudi Arabia may want to think

about de-pegging would be to prop up revenue as a devalued Riyal would be a

great welcome boost. The Saudi oil minister Ali al-Naimi was ousted on Saturday

07/05/16. Mr Naimi had led calls to help re-balance the struggling oil market so

his removal may indicate a slower price recovery.

5.

Watch the 2nd quarters

US earnings trends. If earnings continue to slip into the second quarter,

things could get ugly for US Stocks.

As Preston, of Investors

Podcast noted, US reporting data from quarter 1 was terrible. Fundamentally,

growth continues to slow in the US, corporate profit margins continue to

decrease and international markets continue to struggle (particularly the Bank

of Japan, the PBOC, and European Banks). Although the market could even

run higher, the upside to downside risk/reward continues to be asymmetrical.

6.

Brexit: This

could be a big concern for trade and US stocks.

Instability

due to an exit of Britain from the EU would be a real concern. The June 23rd

referendum is one

that all eyes are eagerly going to be watching soon.

7.

High yield

debt. The oil industry supposedly has 3 trillion or more in debt with as

much as 50% being estimated as junk. Some really interesting things could

happen here if global demand continues to slip in energy and prices start

heading lower again. I think this is a major concern moving forward, but

there is no way of knowing if this trend will return for sure.

Some expect

that this trend will continue but it could go the other way as well. Oil prices are showing some signs of recovering but Iran's recent stint to crank up production may compel Russia and the Saudis to ramp up production as well. These actions would go some way to reverse the current upward trend.

Reference links provided within the post in grey.